Check out our annual 2023 Year in Review, an economic and market commentary with Chief Investment Officer Matthew Harbert, Senior Wealth Advisor Drew Allen, CFP®, CLU®, CEPA, ChFC®, RICP®, and CEO David S. Silver, CFP®, CEPA® from Instrumental Wealth.

Play the video recording, or see the transcript below organized by section & topic. Each topic has screenshots from the presentation.

Table of Contents:

- Crisis in the Banking System (0:53)

- Did the Fed Succeed? (2:10)

- U.S. Credit Downgrade (3:30)

- Inflation & FOMC Interest Rate Policy (4:20)

- How the Markets did in 2023 (7:08)

- Portfolio Changes - Adding Alternatives (10:14)

- Portfolio Changes - Adding Exposure to Private Markets (10:49)

- Portfolio Changes - Private Credit Trends & Benefits (16:40)

- Tactical Positioning in the Portfolio (18:26)

- Benefits & Detractions in 2023 (20:40)

- 2024 What to Expect (22:58)

Crisis in the Banking System (0:53)

All graphs and charts are for illustrative purposes only.

Multiple Bank Failures:

The banking crisis in 2023 was marked by the collapse of several banks, starting with Silicon Valley Bank in March, followed by Signature Bank and later First Republic Bank, which was rescued by JP Morgan.

Fear of Financial Contagion:

These failures sparked widespread fear of a potential financial contagion similar to the 2008 financial crisis, raising concerns about the stability of the banking system.

Federal Intervention:

In response, the Federal Reserve (Fed) took decisive steps to mitigate the crisis, including guaranteeing depositor funds and creating a funding program for banks to ensure liquidity and prevent further collapses.

Did the Fed Succeed? (2:10)

All graphs and charts are for illustrative purposes only.

Effective Stabilization Measures:

The Federal Reserve's interventions appeared to successfully stabilize the banking sector, as evidenced by the cessation of bank failures after July 2023, limiting the total to four for the year.

Market Stability:

The stability gradually returned to the financial markets, with the banking sector showing signs of recovery as indicated by market performance data, suggesting the Fed's measures effectively contained the crisis.

U.S. Credit Downgrade (3:30)

In 2023, the United States experienced a credit rating downgrade from AAA to AA+ by Fitch, primarily due to concerns over rising national debt and political dysfunction.

Limited Market Impact:

Despite the downgrade, the financial markets largely shrugged off the news, indicating that the immediate financial impact was minimal, though it did tarnish the U.S.'s financial reputation.

Inflation & FOMC Interest Rate Policy (4:20)

All graphs and charts are for illustrative purposes only.

Continued Fight Against Inflation:

The Federal Reserve maintained its aggressive stance against inflation throughout 2023, with inflation rates decreasing from 7.04% to 3.35% by the year's end.

Interest Rate Hikes:

The Fed completed its rate hiking cycle, increasing rates by a total of 525 basis points, the fastest and most significant tightening cycle in history, and hinted at potential rate cuts starting in 2024.

How the Markets Did in 2023 (7:08)

All graphs and charts are for illustrative purposes only.

Equity Market Recovery:

Despite volatility throughout the year, the equity markets ended 2023 on a strong note, with significant rallies in December influenced by the Fed's policy signals.

Significant Gains in Major Indices:

U.S. markets saw gains of just under 26%, while international developed markets and emerging markets also posted positive returns, although the performance was heavily influenced by a select group of tech stocks, known as "The Magnificent 7."

Bond Market Rebound:

The bond market recovered from earlier losses, closing the year with a positive return, buoyed by the Fed's dovish stance and expectations of rate cuts.

Portfolio Changes - Adding Alternatives (10:14)

All graphs and charts are for illustrative purposes only.

We introduced alternatives, including private equity and income-oriented private real estate, to enhance diversification and potential returns.

These alternatives were added as a strategic move to access growth and income opportunities outside the traditional public markets.

Portfolio Changes - Adding Exposure to Private Markets (10:49)

All graphs and charts are for illustrative purposes only.

Increased Accessibility to Private Markets:

Recent structural changes and the introduction of new investment vehicles have made private markets more accessible to individual investors, prompting their inclusion in the portfolio.

This shift acknowledges the growing importance of private markets in the investment landscape, providing investors with opportunities previously reserved for institutional investors.

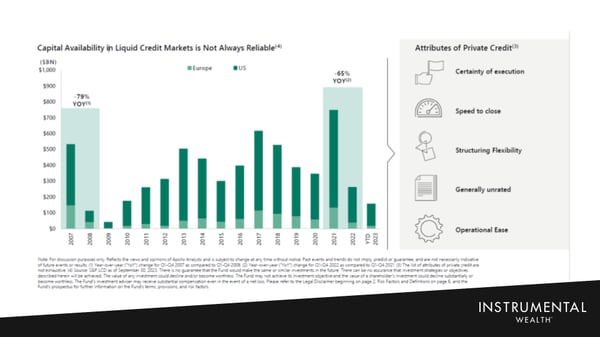

Portfolio Changes - Private Credit Trends & Benefits (16:40)

All graphs and charts are for illustrative purposes only.

Growth of Private Credit:

Companies are increasingly turning to private credit markets for financing due to the flexibility, quicker access to capital, and less regulatory burden compared to traditional bank loans or public bond issuance.

Potential Advantages for Investors:

Private credit offers higher returns and stronger covenant protections for investors, making it an attractive component of the portfolio.

Tactical Positioning in the Portfolio (18:26)

All graphs and charts are for illustrative purposes only.

Adjustments for Market Conditions:

The portfolio underwent tactical positioning adjustments, including overweighting in U.S. large caps, private credit, and fixed income, while underweighting international developed, emerging markets, and real assets.

Strategic Fund Inclusions and Exclusions:

Changes to the fund lineup included adding Pacer funds for higher quality exposure, interval funds for private equity and credit, and thematic investments in clean energy, while removing certain funds that no longer aligned with the portfolio strategy.

Benefits & Detractions in 2023 (20:40)

All graphs and charts are for illustrative purposes only.

Positive Contributors:

Overweights in U.S. large caps and private credit, along with the inclusion of Pacer funds and alternative credit funds, contributed positively to the portfolio's performance.

Areas of Underperformance:

The overweight in fixed income and the inclusion of private equity and thematic investments in clean energy underperformed in 2023, reflecting the challenges in those sectors.

2024 What to Expect (22:58)

Inflation and Interest Rate Outlook:

Inflation is expected to continue its downward trend, with the Fed likely starting rate cuts in 2024, although the extent and timing of these cuts remain uncertain.

Economic Scenarios:

The possibility of a soft landing is considered more likely than a recession, but indicators such as the inverted yield curve and leading economic indicators suggest that the risk of a mild recession cannot be dismissed.

Market Implications:

U.S. equities, particularly large caps, are expected to benefit from potential rate cuts, with a broader market rally anticipated beyond the dominant tech stocks. Fixed income markets are also expected to see positive effects from the easing of interest rates.

Not an offer: This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has sufficient knowledge and experience to be able to understand and make their own evaluation of the proposals and services described herein, any risks associated therewith and any related legal, tax, accounting or other material considerations. To the extent that the reader has any questions regarding the applicability of any specific issue discussed above to their specific portfolio or situation, prospective investors are encouraged to contact Instrumental Wealth or consult with the professional advisor of their choosing.Forward-looking statements: Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.Past Performance: There is no guarantee that the investment objectives will be achieved. Moreover, the past performance is not a guarantee or indicator of future results.