Click here to view the Custom Marketplace Update [PDF].

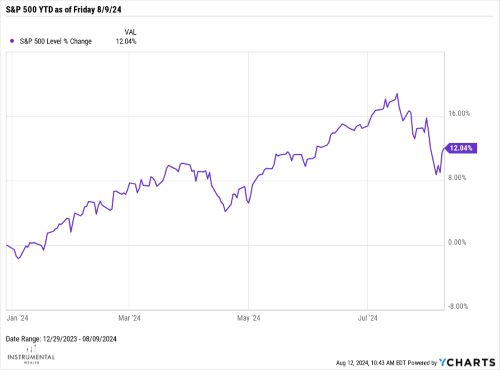

The S&P 500’s volatile performance last week reflected some economic concerns and market dynamics. On Monday, the index was rocked by a sharp sell-off, triggered by a weaker-than-expected U.S. jobs report. The Labor Department's data showed that job growth had slowed more than anticipated and the unemployment rate’s increase triggered the Sahm rule, raising alarms about a potential recession. This was compounded by the unwinding of yen carry trades, following the Bank of Japan’s surprising decision to raise interest rates. This move caused a ripple effect in overall global markets, intensifying the sell-off in the U.S.

By mid-week, however, the S&P 500 staged a notable recovery, driven by stronger-than-expected U.S. services data and a drop in initial jobless claims.

The Institute for Supply Management (ISM) reported that the services sector expanded more than expected in July, which helped ease some of the recession fears. With the survey rising to 51.4 from the 48.8 June result, it puts the services sector of the economy back into expansion territory. "The increase in the composite index in July was driven by an average increase of 5 percentage points for the business activity, new orders, and employment indexes. The one subcomponent that was down was the supplier deliveries index, which fell by 4.6-points.

Source: Institute of Supply Management

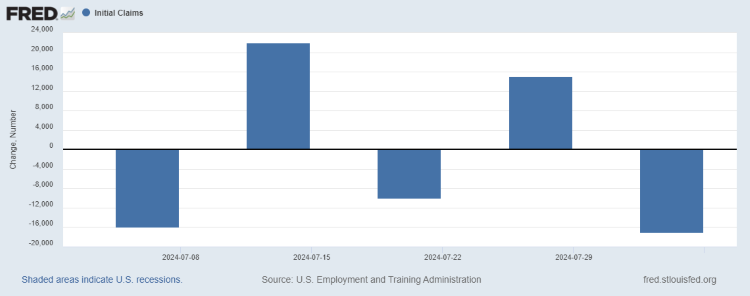

Additionally, weekly jobless claims fell, slightly easing some jitters brought on by the unemployment rate from the previous week. The report showed that initial claims fell by 17,000, beating estimates by 7,000 claims. However, the results have been quite volatile over the past month as they alternated between up and down weeks during that time. In addition, the 4-week moving average number of new claims increased slightly from 238, 250 claims to 240,750 claims.

These positive economic indicators fueled rallies on Tuesday and Thursday, helping the S&P 500 limit its losses for the week to just 0.02%.

Last week’s volatility in the S&P 500 underscores the broader challenges facing the current economy. Investors are navigating a landscape where positive economic indicators are tempered by other key indicators that are pointing to a slowdown of overall growth. Moving forward, this volatility is likely to continue with the economy slowing down as it progresses through the late stage of the economic cycle, combined with the Fed modifying their interest rate policy to one of easing rates.