Click here to view the Custom Marketplace Update [PDF].

The FOMC will be holding their policy meeting Tuesday and Wednesday this week and while hopes are high that they will initiate a rate cut, the consensus among economists is that they will be holding rates steady. This is also in line with what market participants are pricing in. As we can see in the FedWatch chart there is only a 4% chance of a cut priced in the futures markets and a 95% probability the Fed will keep rates the same.

We also believe that the Fed will keep rates unchanged this week, however, as expectations over a rate cut in September rise, we will be paying particular attention to the statements made by Chairman Powell in his press conference following the meeting for any hints on future cuts. Previously, the statements have been that rate cuts would not be appropriate until they gain greater confidence that inflation is moving sustainably to their 2% target. Following a firming up of inflation in the first quarter, prices have decelerated each month over the second quarter.

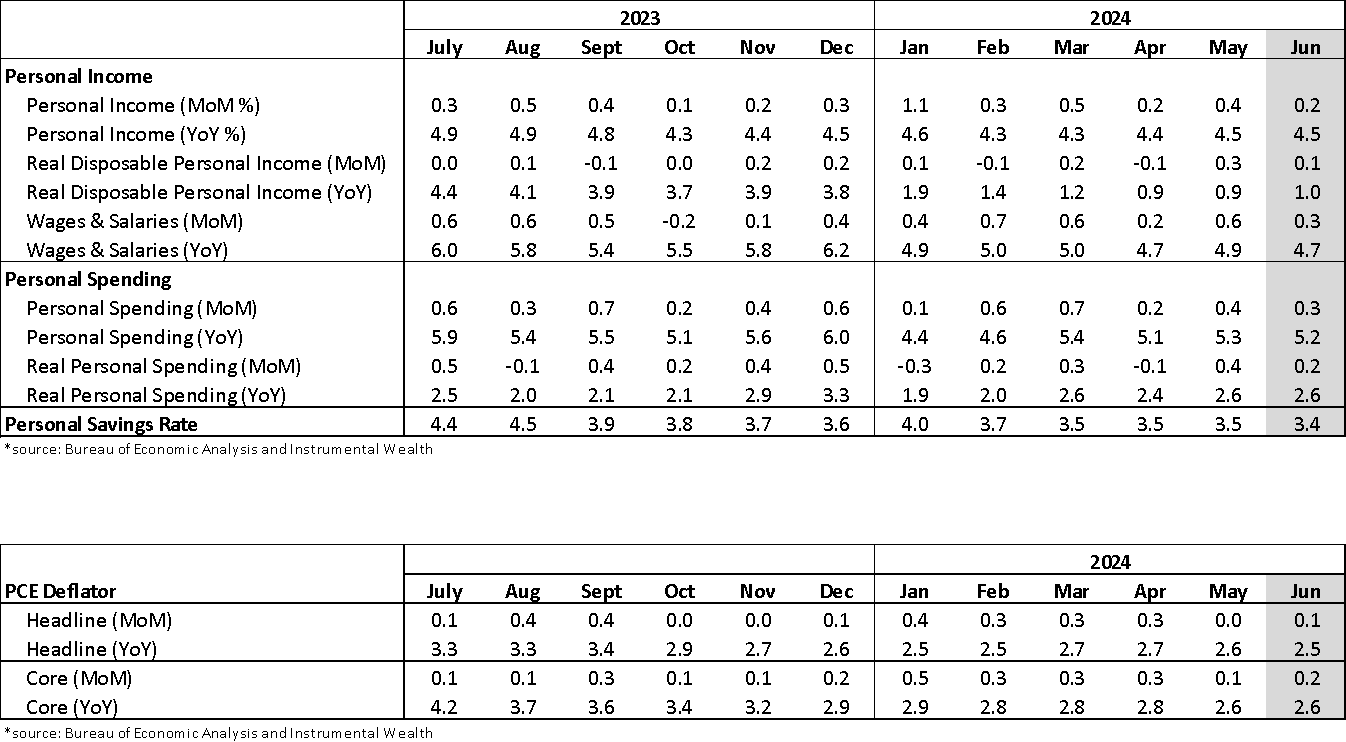

While there is a slight possibility that this would give the FOMC the confidence they need to begin a rate cut as early as this week, the personal income and spending report which came out last Friday will likely keep the Fed waiting for more indication of that “sustained” movement. The report includes the Core PCE inflation index which is the Fed’s preferred inflation indicator. The YoY core number came in unchanged in June at 2.6%. This was slightly higher than the 2.5% rate that economists were expecting, however this may be just a stall as opposed to a reversal the overall trend to that 2% rate policymakers are looking for.

The report also gives us a look at consumers’ overall spending. The results here are what may give the Fed reason to wait for more data. In the month of June there was a .3% increase in personal spending, which is just about middle of the road when comparing to other months in 2024, however, spending in May was revised upwards from .2% to .4%. In addition to the higher monthly rates, the year-to-date number is still coming in at a strong 5.2% and even after adjusting for price increases, spending grew by 2.6%.

Overall, we think the data is moving in a direction that will give the Fed the confidence they need to start bringing down interest rates. The inflation indexes, however, have been volatile this year, heating up in the first quarter and cooling back down over the second, making it more difficult to determine exactly where prices are heading. We believe the Fed will want to see some more proof that this cooling off will be sustainable, however as the Core PCE has stalled this past month and personal spending also firmed up a bit it is unlikely that they will have the confidence needed to cut rates this week.