Click here to view the Custom Marketplace Update [PDF].

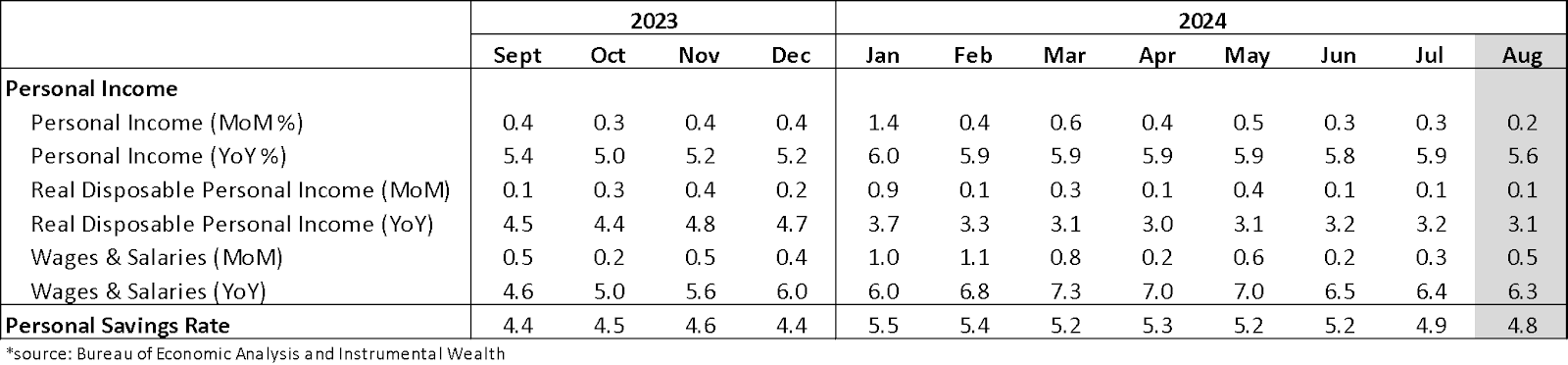

Last week’s U.S. personal income and outlays report was heavily revised, going all the way back to 2019. These revisions implied U.S. households were actually better off than previously thought.

There were upward revisions to both income and savings as real disposable income for households saw significant upward adjustments, meaning that U.S. consumers have been earning more than initially thought. This comes despite downward revisions in the 2023 wage data. Employee compensation was a key driver of these upward revisions, but income from other sources like proprietors' income, rental receipts, and even jobless benefits also saw notable increases.

Income wasn’t the only metric showing improvement from these revisions, the personal saving rate was also revised from sub 3% levels to nearly 5%. This suggests that U.S. households may have more financial cushion than previously estimated, potentially supporting future spending.

While revisions boosted earlier the consumer spending numbers, August data showed a slight moderation. Personal spending grew by 0.2% in August, slowing from July’s 0.5% increase. The deceleration was partly driven by weaker spending on durable goods, including motor vehicles, where higher interest rates may have pushed consumers to delay big-ticket purchases. Spending on nondurables like gasoline also dipped, likely reflecting lower fuel prices. However, spending on services, particularly related to vacations and back-to-school costs, remained robust.

Real personal spending for the year was also revised upward, with July’s spending now 1.2% higher than previously reported, supporting the narrative of strong consumption, even as the third quarter shows some cooling.

Other positive news in the report was on the inflation side. The PCE deflator, which is the Fed’s preferred inflation indicator, continued to moderate in August. The core PCE deflator which excludes volatile food and energy prices, rose by just 0.1% month-over-month, and 2.7% year-over-year. The overall PCE deflator sits at 2.2%, which is very close to the Federal Reserve’s 2% target. With inflation appearing to be under control, the Fed should have more flexibility to shift their focus to the softening labor market.

Overall, the report implies a consumer sector that has been not only resilient but also more financially secure than initially thought. Upward revisions to income and savings paint a brighter picture of household stability, giving consumers more room to support future spending even as inflation moderates and wage growth softens.

While consumer spending growth cooled in August, the overall trend remains positive. Inflation appears to be under control, and early estimates of GDP hint at an economy that is on track for solid growth over the third quarter. In short, U.S. consumers may have more gas in the tank than previously believed, providing a steady hand for the economy.