Click here to view the Custom Marketplace Update [PDF].

This week the FOMC will be meeting, and expectations are that they will cut rates for the first time since they ended the tightening cycle back in July last year. The key datapoints that are expected to drive their decision are a combination of a loosening up of the labor market and an easing of inflation. The labor market, while still healthy, has significantly slowed down, to the point that Chairman Powell stated at Jackson Hole, that we are now at a point that further weakening of employment is a greater risk then rising prices.

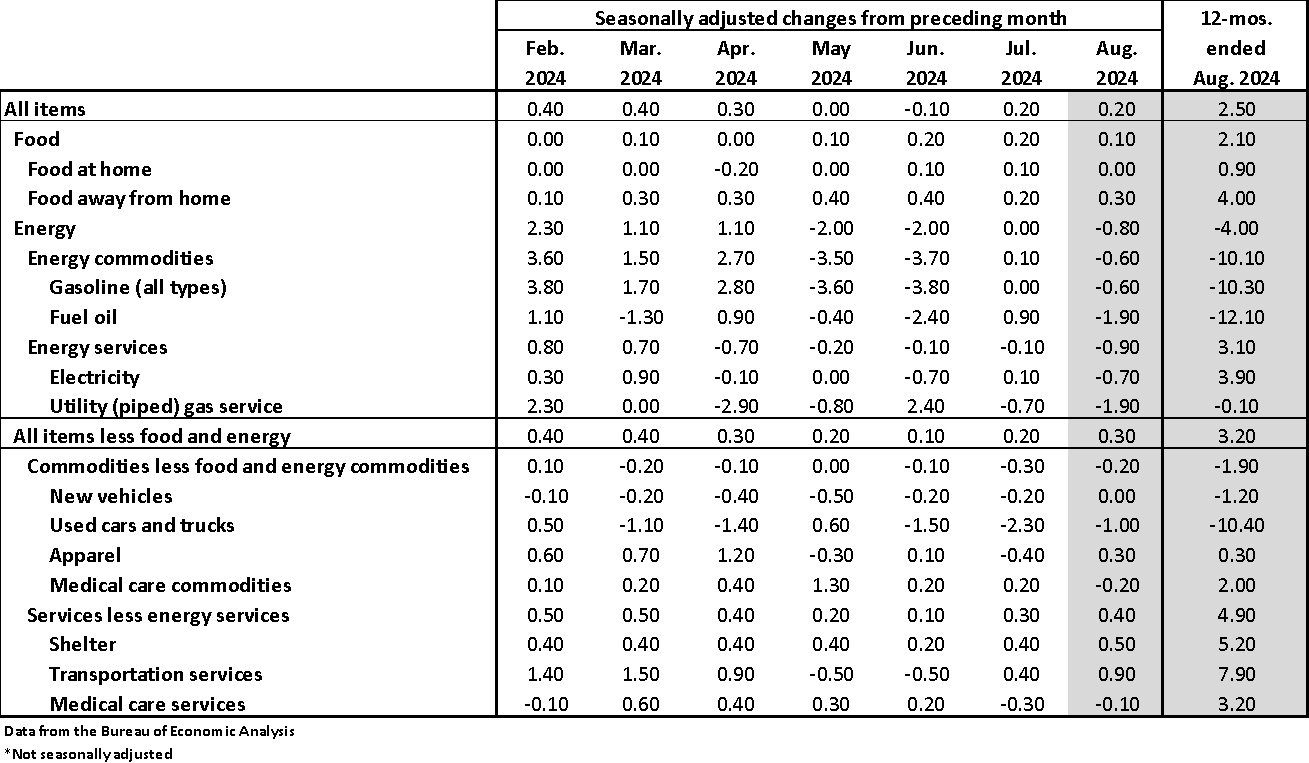

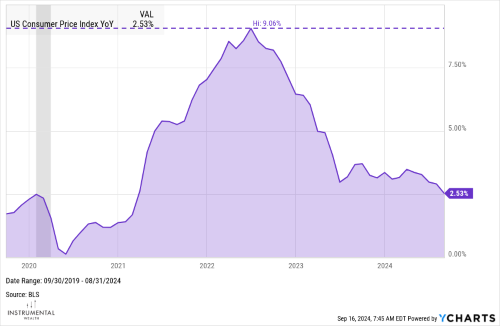

That said, last week’s CPI report was heavily watched for some confirmation that inflation remained at a level that would not spook the Fed away from cutting rates. The results were somewhat mixed, but there was nothing in the report that we feel will stop a rate cut this week. The Headline CPI came in at .2% for the month of August, which was unchanged from July and right at consensus expectations. The year-over-year has come down to 2.53%, which is right around the levels just before COVID hit in early 2020 and very near the Fed’s 2% target.

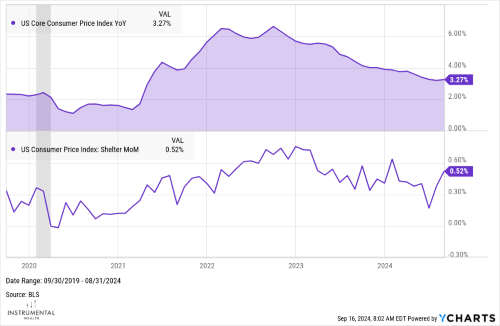

The Core CPI is where challenges remain. For the month of August, Core CPI ticked up slightly from .2% in July to .3% in August and the year-over-year was at 3.2%. This continues to be driven primarily from shelter prices, which make up over a third of the overall index. There was some deceleration in the sector back in June, however shelter prices have firmed back up over the past two months up to .5% in the current month. Transportation services also came in a bit hot at .9% as airline fares spiked to 3.9%.

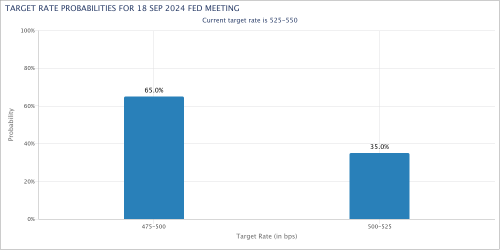

We think it is inevitable that the Fed will go ahead and execute a rate cut this week, the question then is how big the cut will be. There has been quite a bit of talk that the fed will cut 25 bps or even as much as 50 basis points. The markets have bounced around wildly over the past week, according to CME’s FedWatch, they were pricing in about a 15% probability of a 50 bp cut early last week to about a 50/50 percent probability on Friday. Today, however, this probability has increased to 65%. However, with the latest GDP estimate still showing a healthy economy and some important areas of CPI elevated, they may want to start with a modest cut and see how the economy and markets react. We think a 25 bp cut is more likely, but it would not be a big surprise if they go with a 50 bp cut, the significance will be more that the rate cutting cycle has started.