Trump Accounts became available on July 4, 2026, almost a year after the One Big Beautiful Bill created them. We covered these accounts briefly last October as one of five tax opportunities in that legislation, and I recorded the video below, walking through the basics not long after the bill passed. Now that money can actually move into these accounts, it made sense to come back with more detail on how to open one, who benefits most, and what the tax picture looks like over time.

What a Trump Account Is

A Trump Account is a new tax-advantaged investment account for children under 18, created under Section 530A of the tax code. Think of it as an IRA built for kids, with a parent or guardian acting as custodian until the child turns 18. Unlike a 529 plan, the money isn't tied to education expenses. Once the account converts and the child gains control, the funds can go toward a home, a business, retirement, or anything else. That flexibility sets it apart from both a 529 and a custodial UTMA, which comes with its own tax quirks around a child's unearned income.

Opening an Account

Parents or guardians request an account through IRS Form 4547, either when filing a tax return or through the online portal at trumpaccounts.gov. The IRS reported that more than 4 million children already had elections on file before the accounts opened, with over 1 million tied to the federal seed contribution.1 Once the account is set up, the responsible party manages investments and rollovers until the child turns 18, at which point control shifts to the beneficiary.

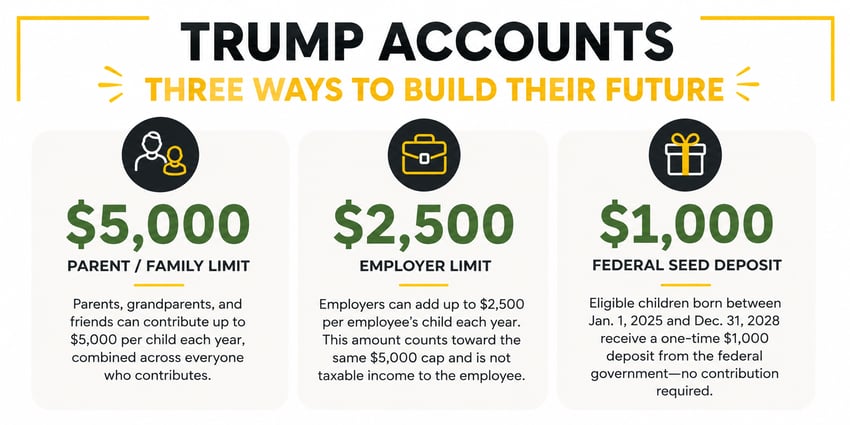

Contributions and Free Money on the Table

Parents, grandparents, and friends can contribute up to $5,000 per child each year, combined across everyone who contributes. Employers can add up to $2,500 per employee's child, and that amount counts toward the same $5,000 cap without counting as taxable income to the employee. Eligible children born between January 1, 2025 and December 31, 2028 also qualify for a one-time $1,000 seed deposit from the federal government, no contribution required.2 A few companies have already stepped in with matching commitments. Micron pledged $250 million to the effort just before launch,5 and Treasury has said more corporate and philanthropic support is likely. Contributions have to happen within the calendar year, so unlike an IRA, there's no extension into the following April.

Where the Money Goes

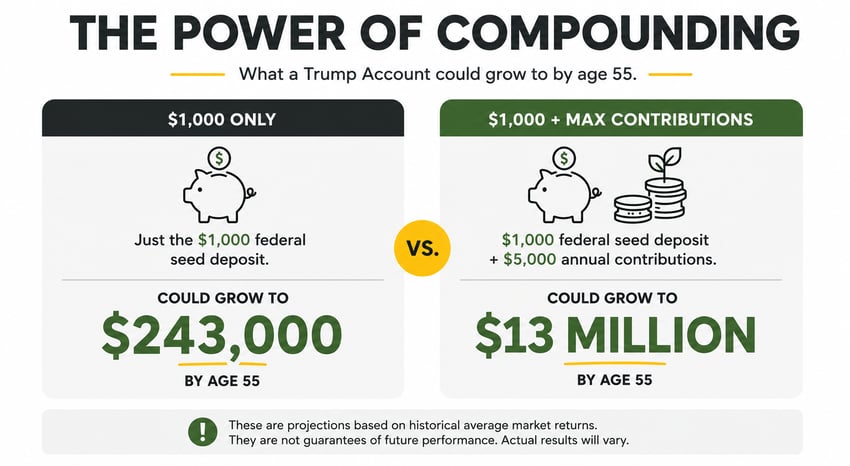

Treasury set the default investment as SPYM, a low-cost S&P 500 index ETF from State Street, and accounts are required to stick to index funds with expense ratios of 0.10% or less.3 Treasury's own projections at trumpaccounts.gov show a child who receives only the $1,000 seed deposit and nothing else could see the account grow to roughly $243,000 by age 55, assuming historical market returns hold. Add the full $5,000 annual contribution on top of that, and the same projection puts the balance closer to $13 million by age 55.4 Those figures depend entirely on future market performance and consistent contributions, but they show what compounding over five decades can do.

Taxes Now and Taxes Later

Contributions are made with after-tax dollars, so there's no upfront deduction the way there is with a traditional IRA. The money grows tax-deferred while the child is a minor. Once the child takes control at 18, the account is treated like a traditional IRA. Withdrawals before age 59 and a half generally trigger income tax plus a 10% penalty, with the usual IRA exceptions for a first home or higher education.2 Left alone, the account keeps growing tax-deferred until retirement.

An Opportunity for Employers

Business owners have a reason to pay attention here beyond their own kids. Offering a Trump Account contribution as part of an employee’s potential benefits lets a company add up to $2,500 per employee's child, take the deduction,2 and hand employees something tangible that a lot of competitors aren't offering yet. In a hiring market where every advantage counts, this is a low-cost way to stand out.

What We're Still Waiting On

The IRS has issued Notice 2025-68 and a round of proposed regulations, but some details remain open, including how these accounts interact with estate and gift tax rules for larger family contributions.2 Treasury already smoothed one wrinkle with a gift tax reporting safe harbor for individual donors,6 and more guidance is expected later this year. If a grandparent or other relative is considering a larger contribution, that's a conversation to have with us before moving money.

Taking Action

If you are considering opening an account, we recommend opening it as soon as possible even if you can't contribute the full amount right away. The $1,000 seed deposit doesn't require you to put in a dime yourself, and every year you wait is potential growth you don't get back. If you run a business, ask us how a matching contribution might fit into your potential benefits package. And if grandparents or other family members want to contribute more than the standard limit, let's talk through the current rules together first.

Reach out to our team to talk through where a Trump Account fits into your family's or your company's plan.

---

Sources

1. Internal Revenue Service, “4 million children have been signed up for Trump Accounts with 1 million claiming the $1,000 pilot program contribution,” IRS.gov newsroom, July 2026. https://www.irs.gov/newsroom/4-million-children-have-been-signed-up-for-trump-accounts-with-1-million-claiming-the-1000-pilot-program-contribution

2. Internal Revenue Service and U.S. Department of the Treasury, Notice 2025-68 and related guidance on Trump Accounts, including contribution limits, eligible investments, and tax treatment, IRS.gov, December 2025 through July 2026. https://www.irs.gov/newsroom/treasury-irs-issue-guidance-on-trump-accounts-established-under-the-working-families-tax-cuts-notice-announces-upcoming-regulations

3. CBIZ, “Trump Accounts Launch July 4, 2026: Key Timing, Estate, and Gift Tax Implications,” cbiz.com, June 2026. https://www.cbiz.com/insights/article/trump-accounts-launch-july-4-2026-key-timing-estate-and-gift-tax-implications

4. CNBC, “Trump Accounts for kids launch July 4: What parents need to know,” cnbc.com, July 1, 2026, citing U.S. Treasury and trumpaccounts.gov growth projections. https://www.cnbc.com/2026/07/01/trump-accounts-launch-july-4.html

5. Micron Technology, Inc., "Micron Announces $250 Million Investment in Trump Accounts Reaching 1 Million Children, Families and the Future Workforce," news release, June 30, 2026. https://investors.micron.com/node/50701/pdf

6. U.S. Department of the Treasury and Internal Revenue Service, gift tax reporting safe harbor guidance for individual Trump Account contributions, announced June 29, 2026. Referenced via IRS.gov and Treasury Department public statements.

This article is for informational purposes only and should not be construed as legal or tax advice. Please consult with qualified professionals regarding your specific situation.

Instrumental Wealth is an investment adviser in Tampa, Florida. Instrumental Wealth is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. A copy of Instrumental Wealth's current written disclosure brochure is available through the SEC's website.

Not an offer: This document does not constitute advice or a recommendation or offer to sell or a solicitation to deal in any security or financial product. It is provided for information purposes only and on the understanding that the recipient has knowledge and experience to understand and make an evaluation of the information, the risks associated therewith, and any related legal, tax, or other material considerations. To the extent that the reader has any questions regarding the applicability of this information to their specific situation, they are encouraged to contact David Silver or consult with the professional advisor of their choosing.